Taking Another Look At Inflation

Taking Another Look At Inflation

By Christine Cooper and Rohit Diwadkar

CoStar Analytics

June 2, 2021 | 1:30 P.M.

Pandemic Upends Year-Over-Year Comparisons

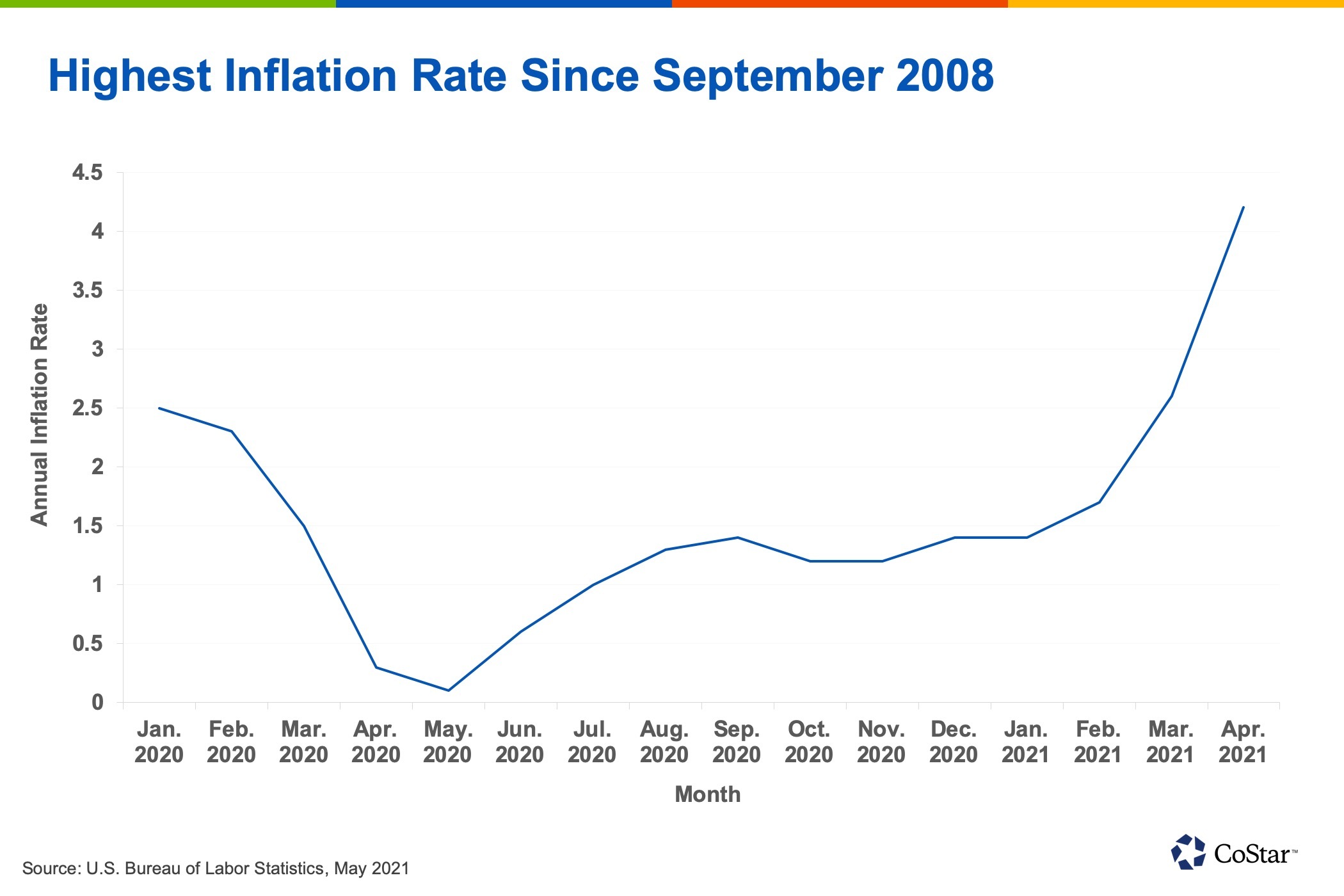

Commentary on inflation pressures abounds these days, especially after the annual inflation rate in the U.S. soared to 4.2% in April from 2.6% in March, well above market forecasts of 3.6%.

The pandemic has upended comparisons based on year-over-year changes because economic conditions a year ago were dire as the economy was shut down to contain the spread of the coronavirus.

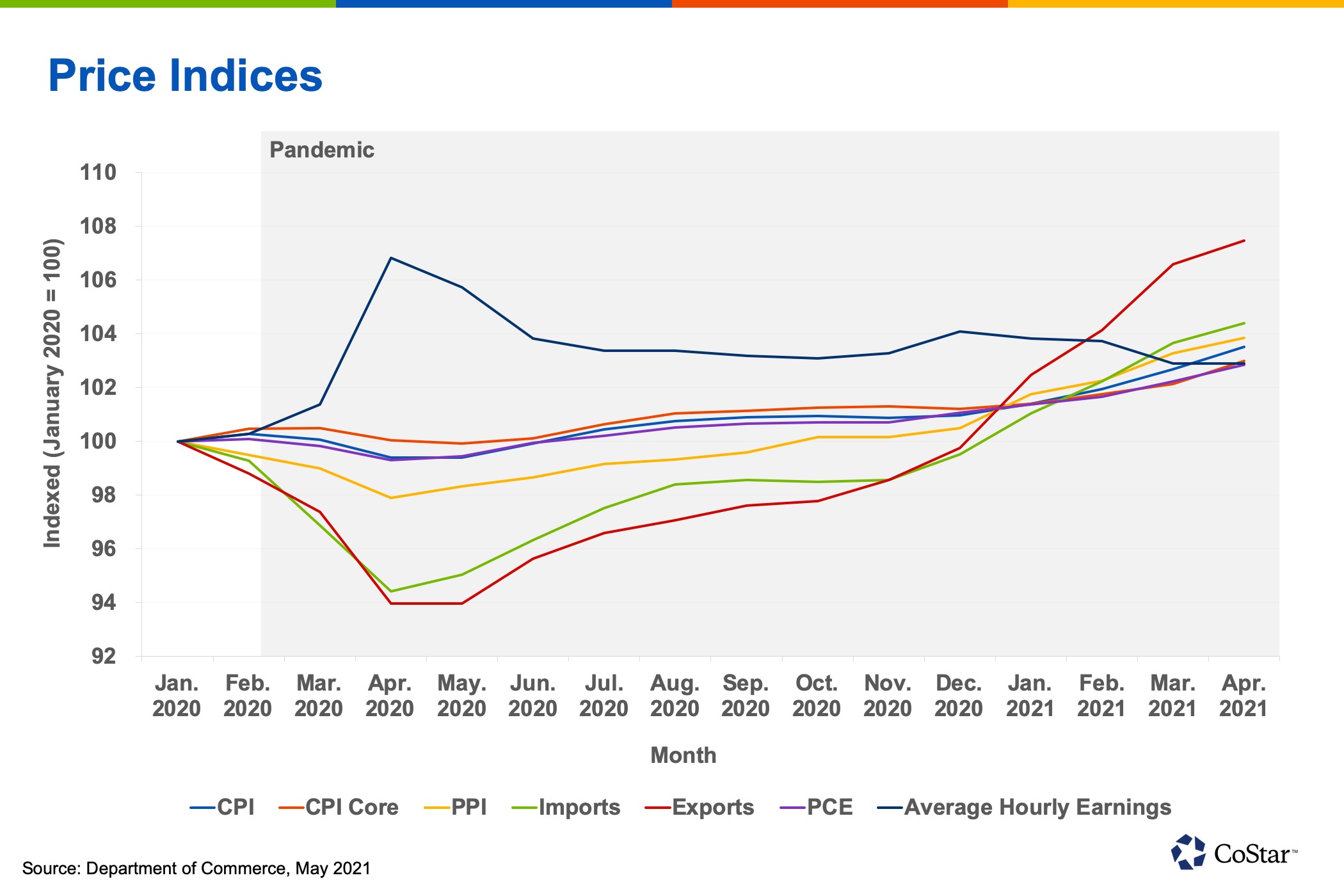

Perhaps a more digestible way to interpret the various inflation gauges is to index each one to its pre-pandemic level in the price indices chart above.

Many prices fell during the first five months of 2020 as the pandemic worsened and economic activity slowed. But by the end of last year, prices had recovered and began accelerating. Recent months have indeed seen higher prices, the largest increase being for U.S. exports.

Most analysts believe that inflation will tick higher this year as unleashed demand bumps up against still-constrained supply. But few see this turning into so-called runaway inflation as expectations of higher prices are not yet turning into higher wage demands. As supply chains heal and demand is slowly met, price increases should moderate later in the year.