Invested in Industrial

Invested in Industrial

Intense competition and strong fundamentals are driving industrial sale prices ever higher.

The industrial sector powered through the worst of the pandemic without missing a step — and the outperformance of the sector has only served to stoke investor demand with robust transaction volume and rising property prices.

“Spreads over U.S. benchmark rates continue to be at high levels by historic standards, which will continue to drive capital into the sector,” says Dennis Mitchell, CCIM, senior managing director JLL Capital Markets in Atlanta. “Additionally, property fundamentals remain strong as demand continues to outpace supply by a wide margin. Due to these tailwinds, we expect investor interest for industrial assets to continue to remain strong.”

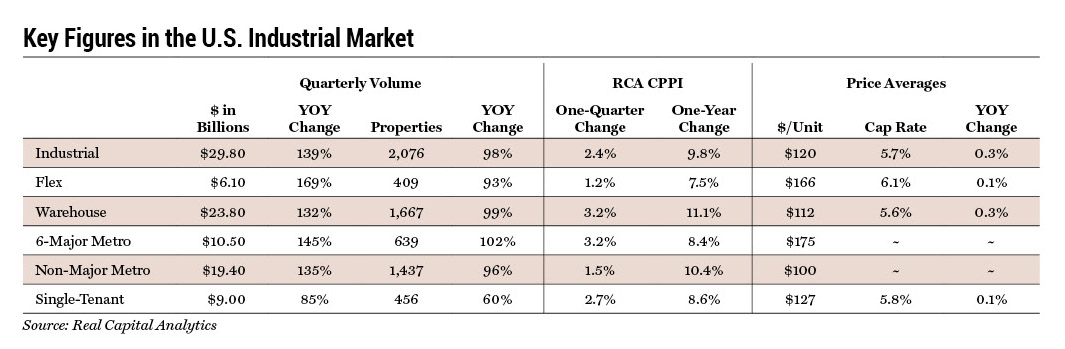

Industrial sales during the first half of 2021 reached $51.9 billion — 10 percent higher than the same period in 2020 and 26 percent above the $38.4 billion in sales recorded during the first half of 2019, according to Real Capital Analytics. Anecdotally, the story is much the same. In Chicago, year-to-date sales through July are tracking about the same or higher than pre-pandemic periods in 2017, 2018, and 2019. “That further proves that industrial continues to perform well despite the challenges of the pandemic, and we think the second half of the year will continue on that same trajectory and finish very strong,” says Adam Marshall, CCIM, SIOR, a senior managing director in the Chicago office of Newmark.

Some large portfolio deals on the market could bolster transaction volumes during the second half of the year. An initial agreement between Equity Commonwealth and Monmouth Real Estate Investment Corp. on a $2.8 billion merger that included roughly 24.5 million sf industrial portfolio was rejected by Monmouth shareholders. However, it also is notable that individual assets account for a big chunk of the sales activity in the market. According to Real Capital Analytics, individual asset sales represented 77 percent of the $29.8 billion in sales that occurred during second quarter. The largest deal to transact in 1H2021 was Costco’s purchase of a 1.6 million-sf distribution facility in California’s Inland Empire from CalPERS for $345 million.

Investors Bullish on Fundamentals

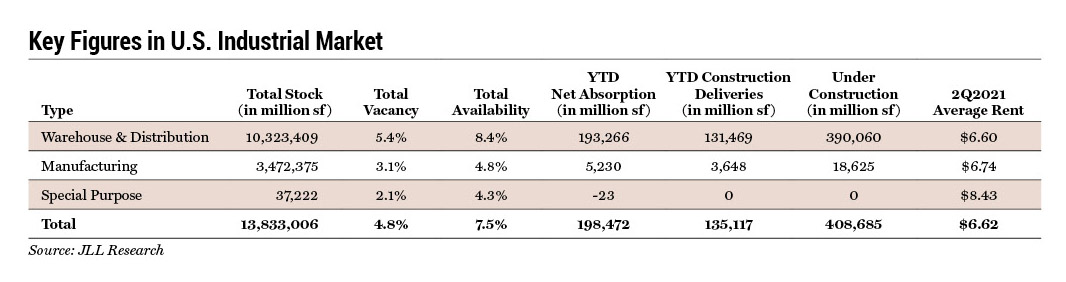

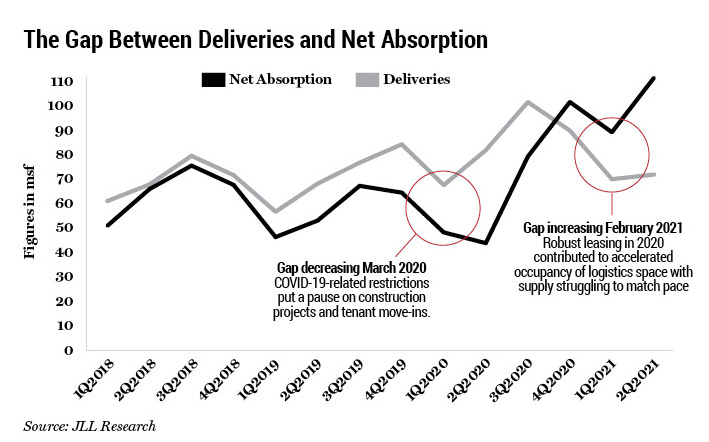

Demand for industrial space surged during the pandemic with a record high of 273.6 million sf of net absorption in 2020. That momentum has carried into 1H2021 with absorption just shy of 200 million sf and vacancies that dipped to 4.8 percent at midyear, according to JLL.

One question is whether 2020 was an outlier with unprecedented demand due to a surge in e-commerce activity. “The pandemic definitely fueled the increase in industrial leasing,” says David Robert Dunn, CCIM, a managing director at SVN Dunn Commercial in Arlington, Texas. Some industry research points to an acceleration of e-commerce during the pandemic that brought growth in online sales forward by about three years. According to the U.S. Census Bureau, e-commerce sales as a percentage of total U.S. retail sales hit a high of 15.7 percent in 2020. Given the broad shift in consumer behavior with more people now comfortable shopping online — even for everyday items — many anticipate sustainable demand for industrial space from the logistics industry. “I don’t think there is any going back,” notes Dunn. “I think we will continue seeing this high demand.”

JLL’s forecast for North American industrial absorption from 2021 to 2022 is anticipated to be healthy at 481.3 msf. At the same time, new supply has surpassed demand two years in a row, something expected to continue over the next two years with new deliveries projected to reach 697.3 msf by the end of 2022. Considering the strong pace of construction, JLL is predicting that the North America vacancy rate will remain low, settling in at 6.2 percent by year-end 2022, which is on par with the 10-year average of 6 percent. “Worldwide, occupier demand for logistics space has never been higher and was also accelerated due to the pandemic,” says Mitchell. “Looking ahead, the industrial sector will continue to thrive for the foreseeable future driven largely by e-commerce growth. Besides e-commerce, future demand is expected to be broad-based from a diverse range of sectors like health care and life sciences.”

Strong demand for space and higher construction costs are pushing rents higher. At midyear, industrial rents were growing at a rate of 5.1 percent year over year, according to JLL. In its second quarter U.S. industrial report, the firm predicted that rents would grow in 2021 and 2022 at an annual rate between 4 to 7 percent.

“Investors are definitely bullish on occupancy and rent growth,” says Marshall. In Chicago, the dwindling supply of space is driving speculative development. Development projects are being impacted by higher land prices in some areas, as well as a roughly 20 percent increase in construction pricing with costs that ultimately will be passed through to tenants, he says. “So, you have all of these forces that will support continued rent growth for the next six to 12 months,” he adds.

Where Is Capital Flowing?

Investment capital remains keenly focused on major logistics hubs serving ports, rail, and air. A quarter of all industrial transactions during the first half of the year were concentrated in five markets. Los Angeles was the most active for industrial sales with $3.2 billion in sales, followed by California’s Inland Empire, Chicago, Houston, and Atlanta rounding out the top five, according to Real Capital Analytics. Investors also are expanding in metros that are experiencing population and job growth. For example, Dallas-Fort Worth has been red hot for both leasing and investment sales, notes Dunn. “Pretty much any building that goes on the market sells very fast,” he says.

1031 like-kind exchange investors from the coasts are coming to the Dallas market in hopes of finding more attractive yields. Dunn recently closed on the sale of a 20,000-sf property with a 1031 buyer from California. The property sold for a 7.5 percent cap rate, but the tenant only had 2.5 years left on the lease. If the property would have had five years left on the lease, it likely would have traded at a 7 percent or 6.5 percent cap. That deal speaks to investors’ willingness to take on leasing risk to close deals, adds Dunn.

Investors also appear willing to expand their investment criteria to place capital. For example, some are willing to look at properties built in the 1960s or 1970s with 16- or 18-foot clear heights. However, buyers remain interested in the “story” that a building has to offer as another factor in why it’s compelling, adds Dunn.

Investor strategies run the gamut from stable A properties to value-add repositioning. Some buyers are looking for bigger portfolio deals. At the same time, other investors who want to assemble portfolios one building at a time are willing to buy an asset with some leasing risk at, say, a 7 percent cap, lease it up, and then turn around and sell the portfolio they have accumulated at a 6 percent cap, notes Dunn. “There are three or four of those buyers in the Dallas-Fort Worth market right now, and two who have been very aggressively trying to find buildings,” he says.

Demand for industrial space surged during the pandemic with a record high of 273.6 million sf of net absorption in 2020. That momentum has carried into 1H2021.

Warehouse/distribution, e-commerce fulfilment, and logistics facilities tend to dominate the conversation in industrial. However, investors are active across the spectrum of different types of industrial assets. “Infill Class A attracts the most buyers, but if you have any industrial assets, there is a lot of demand right now,” says Marshall. There also continues to be good sales activity in the flex market — those industrial assets with a higher percentage of office finish. According to RCA, the $10.3 billion in flex property sales that occurred in the first half of the year represent a 27 percent increase in year-over-year transactions.

In addition, the pandemic has spurred more interest in life sciences and health care-related properties. “The pandemic has created a tremendous amount of research activity that is creating demand for life sciences assets,” says Sid Bhatt, CCIM, senior associate with the Patel Yozwiak Group at Marcus & Millichap in Tampa, Fla., who works on industrial property sales in the Southeast. There are life sciences hubs popping up around the country, such as Boston, San Diego, Philadelphia, and Raleigh-Durham, N.C. At the same time, a variety of startups doing R&D are looking for space in a variety of markets. This creates opportunity for investors to convert industrial, flex, or even office space to lab and R&D space that can support demand from these life sciences tenants, he adds.

Capital Trickles Down to Smaller Markets

Although smaller metros have typically been dominated by local investors, competition in secondary markets is prompting regional buyers to look at buying opportunities in tertiary markets. “We’re seeing an influx from outside sources from Detroit, Grand Rapids, [Mich.,] and Chicago that have their eyes on Northern Michigan,” says Steve Poole, CCIM, a vice president at Colliers in Traverse City, Mich. Traditionally, the challenge is that tertiary markets don’t have a deep inventory of institutional quality multitenant assets. Northern Michigan, for example, is serviced from bigger distribution hubs in Detroit and Chicago.

Most of the industrial sales occurring in Northern Michigan have been on sale-leaseback opportunities of single-user assets. There is a little greater risk because of the smaller market. The timeline to backfill a building with a strong A-caliber tenant can take longer in tertiary markets compared to bigger metros where there is an abundance of options, notes Poole. However, cap rates are going to be higher and there is less competition. Current cap rates on single-tenant industrial assets are trading around 10 to 12 percent, he adds.

Many tertiary markets also benefited from the population shift that occurred during the pandemic with more people working remotely. “Northern Michigan is a beautiful area, and we are starting to see population growth as a result of COVID-19 with a huge influx of people who can work remotely,” says Poole. Businesses are following that population. “We’re starting to see more and more companies interested in locating a facility in Northern Michigan to serve the growing population,” he says. The market has traditionally been conservative on spec development, which has resulted in vacancies that remain tight at about 2 percent, he adds.

Investors Battle Competition, Higher Prices

The biggest challenge for investors is finding good buying opportunities as prices continue to move higher and cap rates lower. Some investors are lowering return expectations due to the competitive environment. According to the RCA CPPI, industrial prices climbed 9.8 percent YOY in second quarter, which is second only to apartments at 12 percent. Warehouse property prices saw an even bigger jump at 11.1 percent, but flex properties also notched some notable gains at 7.5 percent.

Investors also are keeping a close eye on development pipelines and potential overbuilding in some markets.

Cap rates vary widely depending on the market, tenant credit, and quality of the asset. On average, national cap rates declined by 30 basis points to hover at 5.7 percent at midyear, according to RCA. Best-in-class assets in high-demand markets are selling for a premium. For example, Class A industrial assets in the Atlanta market are seeing going-in yields in the 3 percent range, notes Mitchell. “Strong rent growth from both contractual escalations and market growth will help investors validate low cap rates,” he says. “Rents are likely to increase as net absorption continues to outpace new deliveries. Until supply catches up or demand in the space market slows, we expect rents to continue to rise.”

One hurdle for investors is that there is far more demand than there are buying opportunities. “The supply of properties for sale is very low, and you have to work hard to convince someone to sell,” says Bhatt. Many industrial owners are simply reluctant to sell. Especially among smaller ownership groups, there is uncertainty on what to do with the money from a sale, he says. Do they pay the capital gains tax, or do they try to find a replacement property to complete a 1031 exchange? Owners are taking advantage of the attractive climate for refinancing industrial assets that allows owners to restructure debt at a low rate and take equity out of a property. “So, for the majority of people, their strategy is to hold assets,” adds Bhatt.

Investors also are keeping a close eye on development pipelines and potential overbuilding in some markets. For example, Dallas-Fort Worth has record levels of new supply coming online, and it remains to be seen how that space will be absorbed. “I think the future is bright for industrial, but the buildings we’re building right now could create some headwinds where we may see some pressure caused by oversupply,” says Dunn. Another challenge is finding industrial land in a good location. In many metros, infill opportunities are few and far between, which is pushing industrial development further out to the fringes.

Despite rising prices, the yields investors are generating continue to stack up favorably compared to other alternative assets. That investor demand is expected to support lower cap rates and higher sale prices in the near term. The challenge for commercial real estate professionals will be sourcing deals in a market where some owners remain reluctant to sell and helping clients to acquire assets in the current competitive market.